Is BNPL still a hot space in Fintech ?

Why Afterpay was sold for $39b by Square -

And why Zip and Klarna might be a great investment opportunity

Buy Now Pay Later (BNPL) firms have created one of the fastest-growing segments in consumer finance, with transaction volumes going from $33b in 2019 to $120B in 2021 and expected to go to $680B in 2025 (representing 12% of all eCommerce sales on goods, where BNPL is currently concentrated).

Last year BNPL transactions accounted for 2% of transactions in e-commerce last year, and super popular by the younger online consumers

What it is

BNPL are point-of-sale installment loans that allow consumers to make purchases and pay for them at a future date. The interest is paid for by the merchant and is easier to get approved for than traditional credit cards or lines of credit and does not affect your credit score.

If a buyer misses the payment they have to pay back interest on the loan depending on the creditworthiness of the buyer. Similar to what happens in the credit card world if you miss a payment.

The benefit to the retailer

increase in sales revenue by enabling the buyer to purchase products that they would otherwise have left due to a higher price tag.

It’s quite expensive to retailers 4 to 9.5% of the product selling price compared to 2% charged by Credit card companies

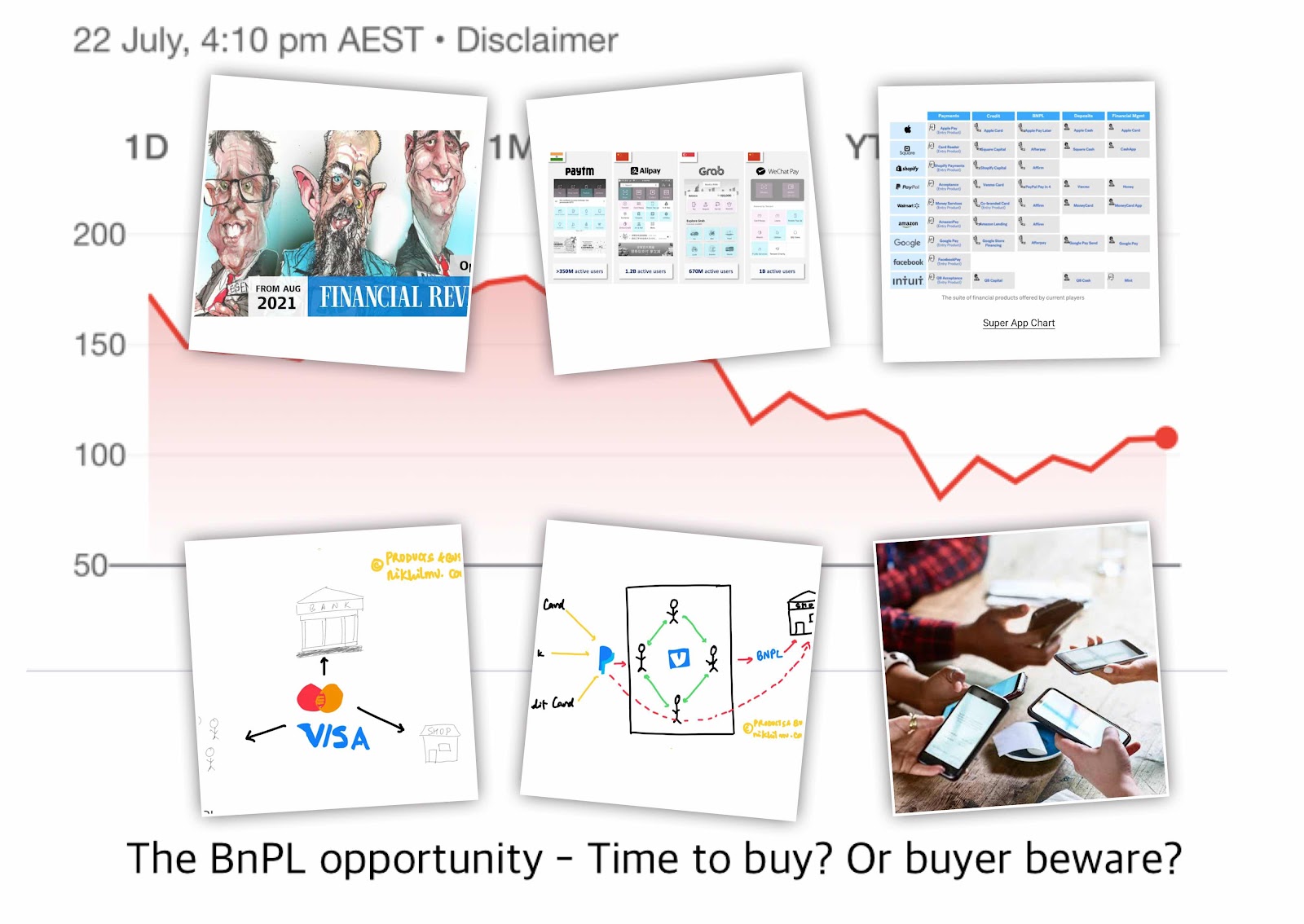

The network effect

Currently credit cards sit between banks, shops and consumers

BnPL ,Cash apps , cryptos and wallets will bypass banks

The PayPal and Cashapp opportunity

PayPal then bought Venmo enabling consumers to pay each other

When Venmo and PayPal will be able to share balances with each other - moneys willing be able to be used to pay the BnpL instalments - without using banks - - a game changer

Same with Square and Cashapp

Risk of BBPL companies

- delinquencies - customers - poor credit quality - 42% lying late - risk mitigation - securitisation of loans

- Regulation enforcing responsible lending practices - BNPL is sending the Gen cycle and z s into a debt spiral

- Entry of Apple and super apps - an unbeatable network effect

- Entry by Legacy Bank

(maybe one of them will buy zip? )

- Klarna which has gone down from $46B in valuation to $6.5B.

- Zip from $3b to $350m

- Block (consolidation of Square and Afterpay has gone from $60b to $40b

Is this a time to buyin??

The super app model will come into this space - but is all about tech integration which companies like Apple and Google can perform easily. Says NIKHIL VARSHNEY https://nikhilmv.com/2022/07/13/three-reasons-why-bnpl-is-failing-the-future-of-bnpl/

No comments:

Post a Comment